What is a Balance Sheet?

A balance sheet is a financial accounting document used to state a company’s current assets, liabilities, and equity. A business should have a balance sheet available in order to show potential investors and shareholders the current financial state of their company. Balance sheets should be updated regularly to reflect the current financial state of the business.

There are two sides to the balance sheet: one will have assets, and one will have liabilities. These two sides should even out for a business to be successful. Each account should be listed separately. The company only needs to list their current assets and liabilities for the particular time period.

Balance sheets will vary depending on the type of business. Accountants are typically best suited to complete and present an accurate balance sheet.

If you're a small business owner, you'll need to learn how to put a balance sheet together. Good news - creating one is not difficult. You can easily create a balance sheet in Microsoft Excel, or Numbers if you are Mac user. Essentially, balance sheets allow you and your shareholders to assess your business' financial status. This article gives you everything you need to draw up a balance sheet template, which you can then fill in with the pertinent information.

Why is a balance sheet so important?

Balance sheets provide an accurate record of a business’ financial status. As long as the company’s balance sheet is up to date, it can provide an accurate snapshot of the company's financial state. Many business owners will generate an income statement to calculate their profit margin and will look at their account transactions, or recent financial statements to ensure the health of their business. However, creating a balance sheet is the best way to accurately calculate any profit/loss margins for your business, as well as ensuring you’ve properly been paid.

We get it. When you own a business, large or small, you’ve got a million other things going on, and spending extra time to create a balance sheet seems like an unnecessary and tedious task that you’d just fine without. However, the invested time is sure to pay off. By creating an accurate balance sheet, you may find that your company is in a different financial status than you may have originally thought.

Components of a Balance Sheet

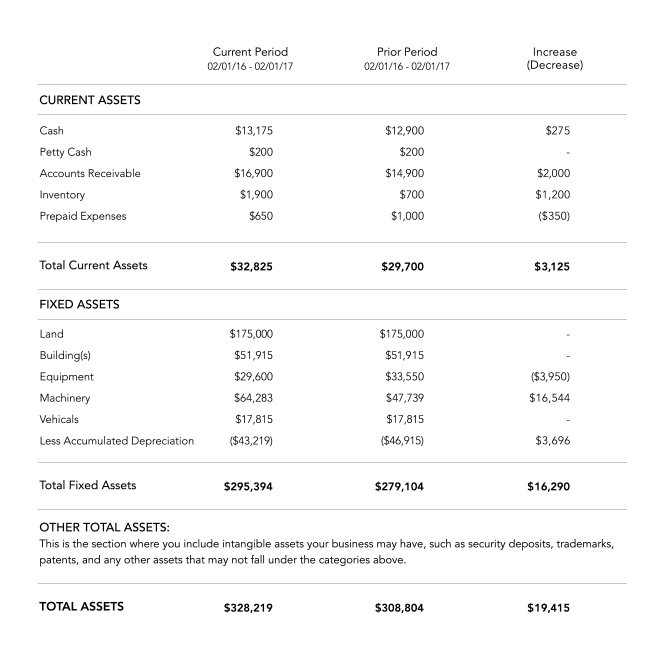

Below are the basic components of a balance sheet, as well as relevant examples to give you a visual of what yours should look like. You can use the information and examples below and input them into your Excel template, or other any other balance sheet spreadsheet you may be using.

Assets

This section includes anything that generates revenue for your business, such as real estate, cash, equipment, and inventory. You should list your assets in two categories - current assets and non-current assets. These are pretty self-explanatory - current assets are assets you expect to use within a year (12 months), such as inventory that you regularly restock. All longer-term assets, such as equipment, company cars, and real estate, fall under the umbrella of non-current assets.

Liabilities

Similar to how assets illustrate financial influx, liabilities reflect outflow and debts your business accrues. Be sure to list total liabilities that are both current (relevant within 12 months) and non-current. Current liabilities generally include short-term loans, purchases, and accounts payable, whereas non-current liabilities are things like long-term loans and mortgages.

The Balance Sheet Formula

The traditional balance sheet formula is important because it helps businesses and shareholders better understand the company’s overall financial health. To acquire assets, businesses must have money to purchase them. Of course, credit is also an option. For many businesses, getting the money to purchase required assets either comes from a loan or from shareholder equity. Taking out a loan or even a line of credit is a liability because it must be paid back. Shareholder equity is money that is invested by shareholders. When the business generates revenue that exceeds their total amount of liabilities, the additional revenue is placed into the shareholder equity account.

Assets, Liabilities & Shareholders’ Equity

-

Assets. Assets can include a number of things. They may or may not be liquid. They may also be considered current assets or non-current assets. Current assets include both cash and cash equivalents. Both accounts receivable and inventory are also considered current assets. Non-current assets include plant, property, and equipment (notated on many balance sheets as PP&E). Intangible assets, such as intellectual property, are also considered non-current assets.

-

Liabilities. Much like assets, liabilities may be current or non-current. Current liabilities include accounts payable. Loans and lines of credit are examples of accounts payable. Balance sheets commonly notate accounts payable as AP. The current portion of long-term debt and certain notes payable that do not qualify as accounts payable are also considered current liabilities. Non-current liabilities include the amortized amount of any bonds issued by the company and certain types of long-term debt.

-

Shareholder equity. Shareholder equity includes share capital for the shareholders and retained earnings of the company.

How a Balance Sheet is used in Financial Analysis & Modeling

A balance sheet is an important document that is compiled to determine the financial health of a business. It allows shareholders to understand the company’s assets compared to its liabilities. It also shows what the company has total after liabilities and shareholder equity is subtracted from assets.

The Limits of a Balance Sheet

One of the limits of determining the financial health of a business using a balance sheet is that it only showcases financial information for a specific amount of time. It can be difficult to get a full picture of financial health for a business based off just one limited time period. Another limitation of balance sheets is actually in how accounting takes place in a business. It is possible for businesses to manipulate the numbers to make the information seem better than it really is.

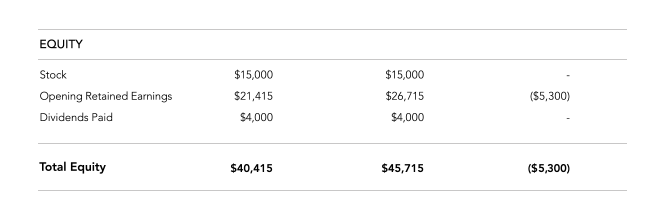

Equity

This final section of your balance sheet reflects the difference between your business' liabilities and assets, also known as owner's equity - in short, what you end up with at the end of the day. It is also known as capital, member's funds or shareholder's equity. When calculating your equity, be sure to factor in assets you yourself have contributed to the business (" capital ",) as well as reinvested profits (known as "retained earnings" or "accumulated losses") and profits set aside for business maintenance, (emergency funds, etc).

What Other Documents Do I Need Along With a Balance Sheet?

What Other Documents Do I Need Along With a Balance Sheet?

Two important documents, in addition to the balance sheet, that aid business owners are the income statement and the cash flow statement. These two documents, when paired with the balance sheet provide a clearer “big picture” of the company’s health, and offer a more accurate, in-depth synopsis of company finances, and in-turn, help owners make sound financial decisions.

A cash flow statement essentially transforms the company ledger and assigns cash inflows and outflows into the following categories:

-

Cash Activity from Financing: This category accounts for the raising of money to run the business and paying it back. Supplying common stock is considered a cash inflow, and repaying the loan is considered a cash outflow.

-

Cash Activity from Investing: The term investing is used to describe the buying and selling of assets. If a business pays cash for investments such as machinery, tools, and equipment, that is considered cash outflow. If any of these materials are sold for cash, that's considered cash inflow.

-

Cash Activity from Operations: This is often referred to as the “miscellaneous” category or the “everything else” category. Every cash transaction that is unrelated to the company's financing or investing is listed in this category. Examples of what would be listed here are expenses such as employee payroll, and assets like payments received from customers.

A company’s cash flow can be calculated with this formula:

(Beginning cash balance) plus or minus (cash inflows and outflows for the month) equals (ending cash balance). It should also be noted that if your numbers are accurate, the ending cash balance will be the same number on your balance sheet.

The income statement is like a close cousin to the balance sheet. The income statement is a very straightforward report on a business’ cash generating power. For example, if a business earned a 15% profit on $100,000 in sales for the month, the income statement will show they earned a $15,000 profit. When a business owner completes his balance sheet, this month’s income statement will be included in the company’s total equity balance.

What is Financial Analysis?

Financial analysis is a step used by many business owners to help calculate their “bottom line”. In other words, it helps business owners calculate their financial situation, and how much it costs them to keep their doors open. In a way, financial analysis exposes the business’ most basic needs, and can also help owners free up extra money each month.

Sometimes, the figure that a company profits each month can be deceiving. Owners may be dazzled that their business profits $1.5 million each month, but that figure is little consolation if they don’t see that it costs them $3 million per month to keep their doors open. Operating expenses need to be paid in cash, regardless if it's up front, or paid at a later date.

Let's take Lisa for example, who owns a clothing company. Lisa’s company generates a 12% profit for every dollar sold. That may sound like a respectable profit, but that means that 88% of every dollar sold pays an expense. $100,000 in sales for the month means $88,000 of that money goes to various expenses. Financial analysis can help Lisa determine her current financial position and as well as aid her in generating more cash every month to pay her expenses more easily. This also helps her reinvest money into her business with the assets she saves. Two common categories that can be adjusted to free up cash each month are: Inventory, and Accounts Receivable.

Inventory

Inventory can be a large expense. Many businesses like Lisa’s rely on inventory to keep sales up. Being out of stock when demand is high only drives customers to go elsewhere, causing sales to drop and Lisa's business to lose money. However, if financial analysis shows that Lisa’s inventory is eating too much of her monthly cash, she can look into other options. If Lisa partners with her suppliers and finds that they can ship smaller quantities of merchandise to her, and expedite the shipping, she can carry less inventory and still meet customer demands--all while saving money each month.

Accounts Receivable

Accounts receivable is money owed to Lisa by her clients. Lisa’s company offers custom attire in addition to items she sells in-store. Sometimes, projects may take weeks to complete. Though Lisa knows her customer will pay once the garment is complete, that money may be weeks away. One way Lisa can increase her cash flow is to offer a discount if customers pay upfront, or if she requires them to pay a deposit up front.

Taking steps to cut back on expenses that rob business owners of cash (such as accounts receivable and inventory) make it easier for business owners to manage their company and cover their expenses.

Conclusion

Though a balance sheet, in addition to its related forms, may seem like a tedious task that only adds to a business owner’s to-do list, it’s a time investment that greatly pays off. With the benefits that accompany creating and maintaining a balance sheet, business owners can be better equipped when making decisions on behalf of their company. With the information and examples in this article, we hope that you have all the tools you need to make an accurate balance sheet, as well as financially analyze your company to potentially free up extra money.

The Personal Balance Sheet Guide for Millenials & a Sample Balance Sheet Template

By FormSwift Editorial Team

March 31, 2021

Introduction

According to the Federal Reserve of New York, as of 2017, borrowing in the US is on the rise. This includes auto, home and credit card loans. The NY Fed found that consumer household debt rose to nearly $13 trillion in the first quarter of 2017. Student loans comprise more than 10% of that sum, meaning Americans currently hold over $1 trillion in student loans.

This guide, therefore, offers a comprehensive review of American household debt, focusing on student loans, household and credit card debt. We cover the causes of debt, key terms to know regarding debt, how to avoid it and how to pay it off. We hope this guide gives you the requisite tools to navigate college and beyond with a detailed understanding of how debt works so you can minimize the amount you take on and pay it off most efficiently.

The Causes of Debt: Common Mistakes

There are many reasons folks find themselves in debt, many of them unavoidable. However, there are a number of common behaviors that drive debt that should be avoided. Those include:

-

Accessing savings and retirement funds too early leaving insufficient capital for retirement and medical emergencies.

-

Insufficient retirement planning, or underestimating the cost of retirement.

-

Poor prioritization of debt payment before retirement.

-

Lack of understanding of the best ways to pay off debt and save money.

Student Debt

According to the Federal Reserve’s Board of Governors, in 2016 the total outstanding federal and private student loans totaled $1.4 trillion. Furthermore, the Pew Research Center found that by 2010, 19% of all US households held outstanding student debt. Even worse, 40% of those borrowers were younger than thirty-five.

In 2017, according to the New York Federal Reserve, the average student loan debt for a borrower after graduation is $34,000.

Key Terms Regarding Student Loan Debt

-

Private student loan debt: loans that a student takes out from private banks, credit unions or online lenders. Private loans typically have the highest interest rates and lack many of the benefits (e.g. forgiveness programs) associated with federal loans.

-

Loan Default: if a borrower does not make their loan payment(s), the student loan will go into default, thereby allowing the lender to begin the collections process.

-

Federal student loans are considered delinquent as soon as a borrower misses a payment. However, the loan servicer will not report the late payment to credit bureaus for 90 days; after 270 days the loan is considered defaulted.

-

Private student loans are considered delinquent as soon as a borrower misses a payment. Furthermore, private loans have no delinquency period. Therefore, private lenders can begin the collections process after a single missed payment.

-

The dangers of defaulting: A default remains on your credit report for seven years and can therefore significantly hurt your ability to rent a home, sign up for a cell phone plan, etc. In addition, those who default cannot lower monthly payments, take out any additional loans, may have their wages and tax refunds garnished, and so forth. Lastly, while you cannot be sentenced to jail for failing to repay a loan, if you are sued by the lender and lose, you can be arrested for not complying with the courts’ summons.

How to avoid default - below are some important tips to help you prevent default:

-

Exhaust all opportunities for free aid—FAFSA, pell grants, etc.—before taking out student loans.

-

Go federal first. Exhaust all available federal loan options before taking out private loans.

-

Create a payback schedule. Budget for how much you need to repay each month and make sure you make your payments.

-

Be proactive. If you think repayment may become a problem, contact your servicer ahead of time and see if there are opportunities to lower or suspend payments.

-

Due to the impacts of the COVID-19 Pandemic, many colleges have restructured financial aid packages to support students in need of relief. Please check out the free SwiftStudent tool to understand all the options you have.

Other important debt relief terms:

-

Repayment rate: the percentage of borrowers who are paying down their loan balance. In other words, the folks not in default.

-

Income driven repayment: a type of payment plan whereby monthly debt payments are capped at a percentage of the borrower’s income. Borrowers who make their payments under this plan for a period of 20-25 years qualify for loan forgiveness.

-

Loan refinancing: refinancing refers to the process whereby existing loans are traded for new private loans at a lower rate. Refinancing at a lower rate can reduce your monthly payments and the amount of interest you pay over the life of a loan. However, be careful when considering refinancing federal loans, which come with repayment flexibility and forgiveness potential unavailable in the private market.

Money habits of responsible borrowers

A key way to make sure you’ll avoid default down the road is to have responsible money habits in place before you take out a loan. Those habits include:

Understanding the most important elements of your personal finance

-

Know your credit score

-

Credit scores affect the ability to get jobs, get loans for a house or make additional deposits for things like a phone line, electric or cable.

-

Credit score vs credit report: a credit score is a numerical value that quantifies an estimate of how likely a borrower is to repay a loan on time. A credit report offers a more in depth report of 7-10 years of an individual's credit behavior and activity.

-

How a credit score is determined: A credit score is calculated using the following formula: 35% payment history, 30% amount of debt, 15% length of credit history, 10% mix of credit, 10% new accounts.

-

Improving your score: Here is a short list of how to improve your score:

-

Diversify your credit accounts

-

Use credit cards every month

-

Never spend above credit card limits

-

Never miss payments

-

Wait at least six months between applying for credit cards

-

-

-

Learn to budget: sticking to a budget helps prevent overspending, plain and simple. If you don’t overspend, you are unlikely to accumulate excess debt. Here are some tips for making a budget.

-

Create a zero-sum budget: Your outgoing money should not surpass your incoming money. Outgoing money includes debt payments, rent, savings, etc. When subtracting all outgoing money from incoming, your end-of-the-month calculation should not be below zero.

-

Create an effective budget: Determine your income or your average income per month if you have an irregular outcome. Track all expenses and categorize them. Create a system for paying bills on time (whether it is through automatic payments or reminders on your phone/calendar), and check and adjust your budget and expenses as necessary.

-

-

Understand investing and retirement options: Having a basic knowledge of how to invest wisely and save for retirement will go a long way to help a student, or anyone, for that matter, understand how to grow their wealth by automatically designating a proportion of income to an investment of some sort.

-

Protect yourself against scams and identity theft: Make sure you have firewalls in place to protect your identity and financial information. Also make sure your cell phones and computer devices are password protected.

-

Understand credit: There are many forms of credit and credit cards. Make sure you make an informed decision when taking out a new line of credit.

-

Things to consider when choosing a credit card:

-

Credit limit

-

Fees

-

Interest rates

-

In general, students should look for a card with a low limit, low fees, and a low-interest rate.

-

-

-

Use credit cards wisely: Credit cards are not for personal indulgence. Instead, you should use your card to build your credit score (only put on a credit card what you can pay off, in full, each month), earn rewards (e.g. cash back, airline miles, etc.), and emergences.

-

Healthy habits for credit cards using include:

-

Paying off your balance in full each month

-

Choose cash instead of plastic when you go out to avoid overspending

-

Avoid impulsive spending, especially on your credit cards.

-

-

-

Avoid, AT ALL COSTS: DO NOT max out your credit limit or charge more money than you can repay before the next payment is due.

Getting out of debt

The goal, of course, is to avoid unwanted debt. However, the financial challenges of life often make this impossible. The amount of money you owe should inform your strategy for repayment. You may decide to pay off debts from smallest to biggest, therefore eliminating interest as quickly as possible. You may, on the other hand, prioritize repayment by interest rate, focusing on the highest rate debt first. Or, you may try to consolidate all of your debt onto a single credit card with a lower interest rate.

Regardless, if you are forced to take on debt, it is important you make a plan to get out of it. Here’s our most important step to get started: Eliminate all unnecessary expenses from a monthly budget.

Debt and college choice

There are many online resources that can assist you in calculating the amount of debt you will need to take on to attend a particular college. Here’s one we like, in part, because it includes federal student loan considerations: https://collegescorecard.ed.gov/.

Paying off debts while still in school

Proactive and financially responsible students often get a head start repaying student loans while they are still in college. Strategies for doing so include:

-

Get a job: Many schools offer work-study positions for students. The extra income will not only help you repay your loans, but they’ll also provide valuable work experience that can help you land a higher paying job upon graduation.

-

Apply for scholarships and grants: There are many scholarships and grants for many different things, not just academic excellence. Research all your school offers in terms of scholarships and grants. Better yet, inquire with someone in the financial aid office.

-

Earn college credit in high school: Students who complete Advanced Placement classes earn college credit. This not only reduces the financial burden of college (fewer credits needed to graduate = less money to graduate), it also boosts your chances of gaining admission into the college of your choice.

-

Even if your school doesn’t offer AP classes, you can take prep courses at local community colleges and sign up to take the AP tests at another location.

-

Paying off student debt vs investing

Many recent graduates struggle with whether to throw as much money as possible at their student loans or invest some of that cash elsewhere. There are benefits to both strategies.

To determine which makes more sense for you, assess the amount of after-tax interest you pay on your debt and compare that to the after-tax rate of return you expect to earn on investments.

Generally, if the return you earn (after taxes) from your investments is greater than the after tax interest rate expense on your debt, it makes more sense to invest than to allocate the extra money to debt payments.

With that in mind, paying off debt first comes with other benefits, including minimizing your tax bill, more protection for your retirement assets, and a shorter timeline to debt-free living.

The latter, for many, is more valuable than whatever small percentage difference you might earn through investing the extra money.

Tips for paying off student debt

Here are our essential tips for paying off student loan debt:

-

Pay off private loans first: They usually have higher interest rates and the least flexibility.

-

Don’t ask for a longer repayment plan: The lower monthly payments of a longer amortization might look appealing, but in reality the longer you take to pay off a loan, the more money you pay in interest.

-

Pay extra: If you find yourself with extra cash, put it towards your debt payments. Typically, money paid in excess of your monthly payment goes entirely to the principle of the loan, which can shorten the repayment period significantly, if done regularly.

-

But don’t overpay: While repaying student loans should be a priority, it should not come at the expense of your financial security. Therefore, make sure you are also saving money, paying off your credit cards, etc.

Student loans and housing

Student loan debt significantly impacts the housing prospects of those in debt. One study found that nearly one in four borrowers took two years longer than those without student loans to move out of their family home. Furthermore, the same study found that 83% of non-homeowners cited student loan debts a major factor barring them from homeownership, and 63% stated that if they had no student loan debt they would use the money they pay towards student loans each month towards purchasing a home.

Things to consider before buying a home

If you have student loans and are considering purchasing a home, recent changes at Fannie Mae, the largest purchaser, and guarantor of mortgages in the US, affect potential borrowers in several ways:

-

If your parent or employer is paying off your debt, that debt no longer counts against your debt to income ratio when you apply for a home loan.

-

Lenders can now use the lower, flexible payment amount that federal student loan recipients may qualify for, which will help more applicants with student loans qualify for a mortgage.

Though these changes should make it easier to qualify for a mortgage, young people with student loans should still consider the following before jumping into homeownership:

-

If your employer or parent stopped paying your debt, would you be able to take on the payment AND afford your mortgage?

-

Do you have enough money for a down payment?

-

Can you afford associated costs with having a home, such as maintenance and insurance?

-

Do you have enough additional money per month to put into an emergency savings account?

If the answer to any of these questions is “no”, consider waiting until you can answer each of these in the affirmative before purchasing.

Student loan debt and mortgages

While it is not impossible to get approved for a mortgage when you have student loans, student loan payments can affect the approval process because your payment history comprises 35% of your total credit score. Therefore, if you fall behind on payments, your credit score will drop and hurt your prospects for mortgage approval. Furthermore, student loans negatively impact your debt to income ratio, a key calculus in the mortgage approval process. Therefore, if you have loans and your income is relatively low, it will be difficult to gain approval. Furthermore, if you are currently struggling to make your loan payments, you should consider how you will save for a down payment and pay a mortgage.

Paying off student debt with home equity

Check out our home loan debt section for a more detailed discussion of home equity. Once you have done so, remember this: taking out home equity loans to pay back student loans a bad idea for multiple reasons:

-

Student loan debts are unsecured and not attached to any collateral like your house. If you transfer these loans to your home's equity you can lose your home in the event you are unable to repay those loans.

-

Federal student loans are eligible for forgiveness programs if you have a hard time paying them off; home equity loans are not.

Sample Balance Sheet with Instructions

A balance sheet is a statement of the financial position of a business; it includes the assets, liabilities, and owners'/shareholders' (stockholders') equity at a certain point in time. A balance sheet is a snapshot of a business's net worth.

A balance sheet lists assets on the left and financing on the right, which includes two sections: liabilities and ownership equity. The difference between the assets and the liabilities is the equity/net worth of the business. According to the accounting equation on which a balance sheet is based, net worth must equal assets minus liabilities:

Assets = Liabilities + Shareholders' Equity

A balance sheet is used, along with other financial statements, such as an income statement and a cash flow statement, in calculating financial ratios, evaluating a business, and making business decisions.

In the assets section, accounts are listed in order (descending) of their liquidity, how easily they can be converted into cash. Total assets are separated into current assets, which can be converted into cash in one year or less, and long-term assets, which cannot.

Order of Current Assets:

-

Cash and cash equivalents, including Treasury bills, short-term certificates of deposit, and hard currency.

-

Marketable securities.

-

Accounts receivable.

-

Inventory, including raw materials and goods available for sale.

-

Prepaid expenses, including insurance, advertising contracts, and rent.

Order of Long-term Assets:

-

Long-term investments that will not or cannot be liquidated in the next year.

-

Fixed assets, including land, machinery, equipment, and buildings.

-

Intangible assets, including non-physical assets, such as intellectual property and goodwill.

The total decrease in the value of an asset on the balance sheet over time is accumulated depreciation. Accumulated depreciation of certain fixed assets is a negative asset used to reduce the value of other accounts. An asset's value on the balance sheet is expressed as the cost of the asset minus accumulated depreciation.

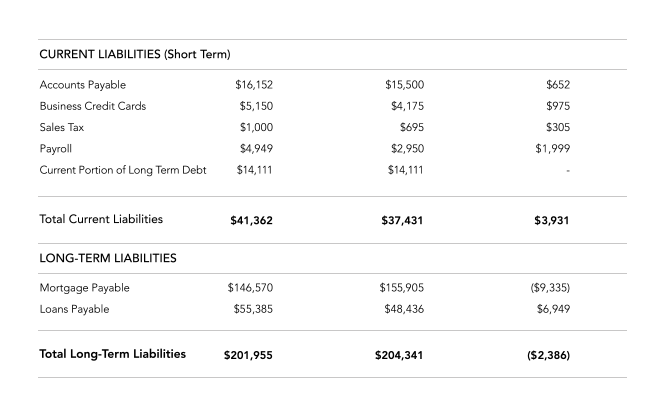

Liabilities, money that a business owes to outside parties, are separated into current liabilities, which are due within one year and listed in order of their due date, and long-term liabilities, which are due at any time after one year.

Current liabilities include a current portion of long-term debt, bank indebtedness, interest payable, wages payable, customer prepayments, dividends payable, earned and unearned premiums, and accounts payable.

Long-term liabilities include long-term debt, interest and principal on bonds issued, pension fund liability, deferred income tax liability (taxes that have accrued but will not be paid for another year, a figure that reconciles differences between requirements for financial reporting and how tax is assessed, such as depreciation calculations).

Working capital, also known as net working capital (NWC), is the difference between a company’s current assets and its current liabilities, such as accounts payable. It is a measure of a company's liquidity.

Shareholders' equity, also known as owners' equity, net assets, or the net worth of a business, is the money that belongs to a business' owners (shareholders); it equals the total assets of a business company minus its liabilities:

Shareholders’ Equity = Assets - Liabilities

Shareholders' equity is the amount of money initially invested into a business plus any retained earnings. Retained earnings are the net earnings a business reinvests in the business or uses to pay off debt; the rest is distributed to shareholders as dividends.

As its name indicates, a balance sheet must always balance.

Sources:

- https://www.investopedia.com/terms/b/balancesheet.asp

- https://en.wikipedia.org/wiki/Balance_sheet

- https://www.investopedia.com/articles/04/031004.asp

- https://www.thebalancesmb.com/balance-sheet-definition-2946947

- https://www.investopedia.com/terms/w/workingcapital.asp

- https://www.freshbooks.com/hub/accounting/is-accumulated-depreciation-current-asset

- https://online.hbs.edu/blog/post/how-to-prepare-a-balance-sheet

Balance Sheet Template:

Household Debt

According to a 2017 study by the National Association of Realtors, US homeownership rates are at their lowest rate in nearly 50 years. However, household debt is still on the rise. Therefore, it is important that homeowners, especially first time buyers, avoid common mistakes people make that often increase their debt.

Tips for first-time homebuyers

-

Understand spending power: Lenders often qualify buyers for mortgage loans based on their debt to income ratio. This, therefore, does not take into consideration any additional expenses like property taxes or homeowners insurance. Often, first-time buyers mistakenly base what they can afford solely on the monthly mortgage payment. Therefore, be sure to factor all these associated costs when determining what you can afford.

-

Get Pre-approved: Pre-approval gives you time to prepare all requisite financial documents before purchasing a home. Therefore, when the time comes to submit an offer, you will be prepared to move quickly which will give you an advantage over other buyers.

-

Know your current credit score: Your credit score helps determine if you qualify for a mortgage as well as the corresponding interest rate.

-

Know your options: There are many mortgage options for first-time buyers. Be sure to do your research and determine which mortgage is best for you. In general, fixed-rate mortgages are the most desirable and responsible option.

Paying off your mortgage

While it may seem obvious that the sooner you pay off your mortgage the better, there are pros and cons to paying off your mortgage early, especially for young owners.

Pros

-

More cash on hand each month

-

No more money going to interest

-

Increased flexibility to take out home equity loans.

Cons

-

The lump sum required to pay off your mortgage may generate a greater return invested elsewhere.

-

Here’s a quick calculation to give you an idea if this might be true: consider the interest rate on your mortgage. Do you think you can earn a higher rate of return investing? If so, you should consider investing that money rather than paying off your mortgage.

-

-

No more mortgage interest tax deduction

-

If you have to borrow against your home you will be right back in debt.

Home equity and home equity loans

Home equity refers to the difference between your home’s value and the amount you paid for it. If your home is worth more than you paid for it, the difference equals your home equity.

Home equity loans and home equity lines of credit are the two types of home equity debt. They are often referred to collectively as “second mortgages.”

Home equity loan: Home equity loans function just like a mortgage. A buyer borrows a lump sum and then repays it in even monthly payments over a fixed-period at a fixed-rate.

-

Home equity loans require a minimum credit score of 620.

-

Home equity loans are appealing for those seeking a large lump sum.

Considerations:

-

If you already have a lot of debt, a home equity loan won’t help; it will simply move debt from one place to another.

-

Home equity loans increase the likelihood you will lose your home. Therefore, if you need a large loan, it may be better to look for other options.

A Home Equity Line of Credit (HELOC): Homeowners borrow money as needed during the “draw period”--typically ten years--and pay either minimum, interest only, payments or larger balances--variable interest.

-

After the draw period ends, the “repayment period” begins and requires monthly payments for 15-20 years, generally.

-

HELOCs function much like a credit card, so they are generally more appealing for buyers who anticipate needing several large sums over several years.

Home equity loans and debt

Think twice before you offer your home as collateral for a loan. If you fail to repay your loan, you risk losing your house. Moreover, if you sell your home, you will have to pay off your mortgage AND any additional home equity loans before you can transfer title to the new buyer.

Home ownership after bankruptcy

Depending on how you file, you will have to wait a certain amount of time before you are eligible for mortgage loans.

-

For example, Chapter 13 bankruptcy may allow for a conventional mortgage after two years; Chapter 7 bankruptcy likely requires four years. Other loans, such as VA or FHA loans, are more lenient.

Buying a Home after Foreclosure: If you lose your home to foreclosure, you typically face a waiting period longer than bankruptcy--seven ears for a conventional mortgage and two to three years for a VA or FHA mortgage.

Foreclosure and Bankruptcy: If both apply to you, you will have to coordinate even more variables and seasoning periods associated with each event.

- Remember, loan qualification is often tied to your credit score. Bankruptcy tanks your credit score so even if your wait period expires, you may not have a credit score high enough to qualify for a loan.

If you do have to file for bankruptcy It is imperative you use the wait periods to rebuild your credit in order to increase your chances of acquiring loans in the future.

Tips for acquiring a bank loan

-

Research your options: By the time you enter a bank, you should have a good idea of what kind of loan you want and how much money you need.

-

Ask questions: Contact banks directly and ask detailed questions about any loan you are interested in and make sure you are eligible.

-

Know your credit history: Have your credit report on hand and familiarize yourself with your credit history. Make sure there are no mistakes. From there, only apply for a loan that you know you can afford and will pay off.

The 2018 GOP tax bill and housing costs

Depending on where you live and the value of your home, the GOP tax bill may have a significant effect on your tax obligations.

Here is a brief overview of changes:

-

Mortgage interest deduction: If you buy a home between now and 2026 you can only deduct interest up to $750,000

-

This is a reduction from the previous limit of $1 million

-

-

SALT deductions: the new bill limits the deduction to $10,000 for both individuals and married couples.

-

This will hurt homeowners in high tax areas like coastal states.

-

Credit card debt

According to the Federal Reserve, America’s credit card debt hit an all-time high in November 2017. Credit card delinquencies also rose over the last year, up to 7.5% from 7%.

A study by Lending Tree found that 42% of respondents cannot pay off their credit card debt because they do not make enough money. Furthermore, 29% cannot pay debt taken out for car repairs, and 27% cannot repay medical bills.

What happens if you don't pay your credit card bills?

The penalties for credit card delinquency vary by the length of non-payment.

-

30 days late: your creditor will likely contact you by phone, letter, or email.

-

60 days late: your creditor will increase your interest rate and you may incur a late fee. Your credit score will also decrease.

-

90 days late: your creditor will likely close your account and you will have to repay the full balance.

-

Note: if your creditor sells your debt to a third party agency they can pursue punitive legal actions.

-

In some states, creditors can sue delinquent borrowers or place a lien on your bank account.

-

-

Credit card debt and credit scores

Your payment history is an essential party part of your credit score calculus. Therefore, outstanding credit card debt can negatively impact your score even if you make regular payments on time each month. To determine this, credit agencies use your “revolving utilization ratio,” which tabulates the relationship between your credit balances and limits.

-

Try this: divide your debt balance by your credit limit. Multiply that amount by 100. The higher the percentage, the lower the credit score.

Biggest problems with credit card debt

Credit card debt should be avoided at all costs. Here are just a few of the problems that come with credit card debt:

-

Credit card debt grows quickly: Credit cards come with high interest rates. Unpaid debt leads to greater interest-related debt which increases your overall debt obligation.

-

Credit card debt hurts your credit score (as discussed above): Furthermore, missed or late credit card payments damage your score further and may remain on credit reports for 7 years.

-

Credit card debt inhibits your ability to save money for the future.

How to lower credit card interest rates

Because of their generally high interest rates, shrewd borrowers should look for ways to lower their interest rates. Here are a few tips for doing so:

-

Balance transfer: Balance transfer credit cards can reduce or eliminate interest charges for a set period of time. However, not everyone qualifies for these cards.

-

Call your credit card company: Have a copy of your recent credit card statements and collect any offers from other companies to use as leverage. Determine a target interest rate that you require to stay with your current company and ask to speak with someone authorized to make such decisions.

-

Personal loans: Personal loans can also reduce your interest obligations.

-

Unlike the high interest rates associated with credit cards, personal loans often have lower rates, especially for those with good credit scores. Your credit score will likely improve because personal loans are unsecured installment loans as opposed to revolving loans like credit cards.

-

-

Focus on debt, not rates: Sure, lowering your rates is ideal, but you should also, perhaps even more so, focus on minimizing the amount of debt you have.

How to pay off credit card debt

Here are our essential tips for paying off credit card debt.

-

Assess your debts and assets: How much money do you owe, in total? How much money do you make each month? How much do you spend each month (and on what)?

-

Make a budget & cut non-essential expenses: Remember, you are in debt because you spend more than you make. In order to climb your way out of debt, you’ll have to start making more than you spend. Doing so requires eliminating all non-essential expenses. If you do not do so, you risk falling deeper into debt.

-

Avoid late fees: Make sure you make at least the minimum payments on your credit cards. Failing to do so will cost you more money and damage your credit score.

-

Even better: Pay off your entire credit card balance each month. Doing so will keep you out of debt and will improve your credit score.

-

-

Keep it below 30%: You should keep your credit balance below 30% of your overall credit line.

-

Make a plan and stick to it: Determine what path towards debt freedom makes the most sense for you and stick to it. That may be paying off debt with the highest interest first, or starting with the credit card with the lowest balance, etc.

-

Ask for help: Contact the creditor and see if they can offer any relief or incentives, like a lower interest rate if you pay off your debt within a certain amount of time.

-

Don’t forget to save: While paying off debt is a top priority, so is saving for emergencies. Therefore, make sure you are still putting a little money away for a rainy day each month.

Savings accounts and credit card debt

As mentioned above, it’s important you have enough in savings to cover emergencies. If you have more than that already put away, consider using some of that extra cash to pay off debts. If you do not have enough in savings to put any towards debt, you should stop using credit cards altogether and focus on paying them off.

Debt consolidation programs

While advertisements for debt consolidation plans online, on television and on the radio are often enticing, BE CAUTIOUS! In general, these programs charge a large fee each month which actually makes it significantly harder to pay off your debt.

Pay off credit card debt or save for retirement?

Which should you prioritize? The answer depends on a host of factors, including:

-

How much money do you have in each?

-

How much money do you owe?

-

How much money have you saved for retirement?

-

How much money do you save for retirement each month? What percentage of your income does that amount represent?

-

Net worth

-

Calculate your net worth if you save for retirement versus if you pay off debt quicker.

-

For each, include credit card balance, APR, proposed annual monthly payment, minimum payment percentage, and minimum payment amount.

-

Credit card debt and the elderly

According to the Demos National Survey on Credit Card Debt and the AARP Public Policy institute, 2012 was the first year in which households headed by people over fifty years old held more debt than households headed by people under fifty.

Why is this the case?

-

Many seniors are still paying off school loans or the loans of their children and may not have saved enough retirement money to cover basic expenses.

-

Medical debt often compounds debt as seniors typically have higher medical expenses than younger individuals.

What can seniors do?

-

Debt counselors can help to organize your finances and put together a payment plan to ensure you do not fall further into debt.

-

Use your savings to pay off high-interest debt.

-

Talk to your medical provider and determine what options you have regarding payment plans for medical bills.

Credit card debt and millennials

Millennials are graduating from college with astronomical student-loan debts which can, therefore, make them vulnerable to credit card debt. It is therefore important that millennials keep the following in mind:

-

Do not be tempted by introductory low-interest rates. They eventually expire and your interest rate will spike.

-

Determine the best credit card for your needs. Be sure that any fees associated with credit cards are absolutely necessary for your financial needs. For example, some credit cards cost hundreds of dollars per year. If you are interested in one of these cards, make sure you will utilize the associated benefits.

-

Keep an eye on your balance and make sure you stay clear of your credit limits.

-

Have multiple cards: This will help you raise your credit score. However, be careful to keep track of each card and do your best to pay off your balance each month.

-

Use your rewards: Many cards offer cash back benefits, airline miles, etc. Utilizing these balances will help you save money down the line.

Conclusion

There you have it. Debt is a complicated enigma that should be avoided at all cost. With that in mind, it is unlikely you will be able to go through life without having to take on some debt, be it through school, home ownership or credit cards. The key to managing debt is to manage it wisely and avoid the variety of pitfalls that drive you deeper and deeper into debt that can seriously harm your financial future. We hope this guide helps you manage your own debt responsibly.

Download a PDF or Word Template

Balance Sheet

In simple terms, a balance sheet is a financial statement. A balance sheet lists the assets, liabilities, and capital of a business during a specified time period.

Income Statement

An income statement is a summary of a business' financial standing for a certain period of time. An income statement lists a company's revenue and expenses over a certain length of time.

Profit and Loss Statement

A profit and loss statement is often referred to as a P & L statement. The purpose of a profit and loss statement is to provide a glimpse at the finances of a business during a certain amount of time. Profit and loss statements are usually created on a quarterly basis.

Personal Financial Statement

A personal financial statement is a breakdown of a person's assets and liabilities. If you're looking to get a loan for a small business, your lender may request that you provide a personal financial statement.